All Categories

Featured

Table of Contents

The are whole life insurance policy and universal life insurance. grows cash value at an ensured rates of interest and likewise via non-guaranteed rewards. expands cash money value at a dealt with or variable price, depending on the insurance company and plan terms. The cash money value is not included in the survivor benefit. Money worth is a feature you capitalize on while active.

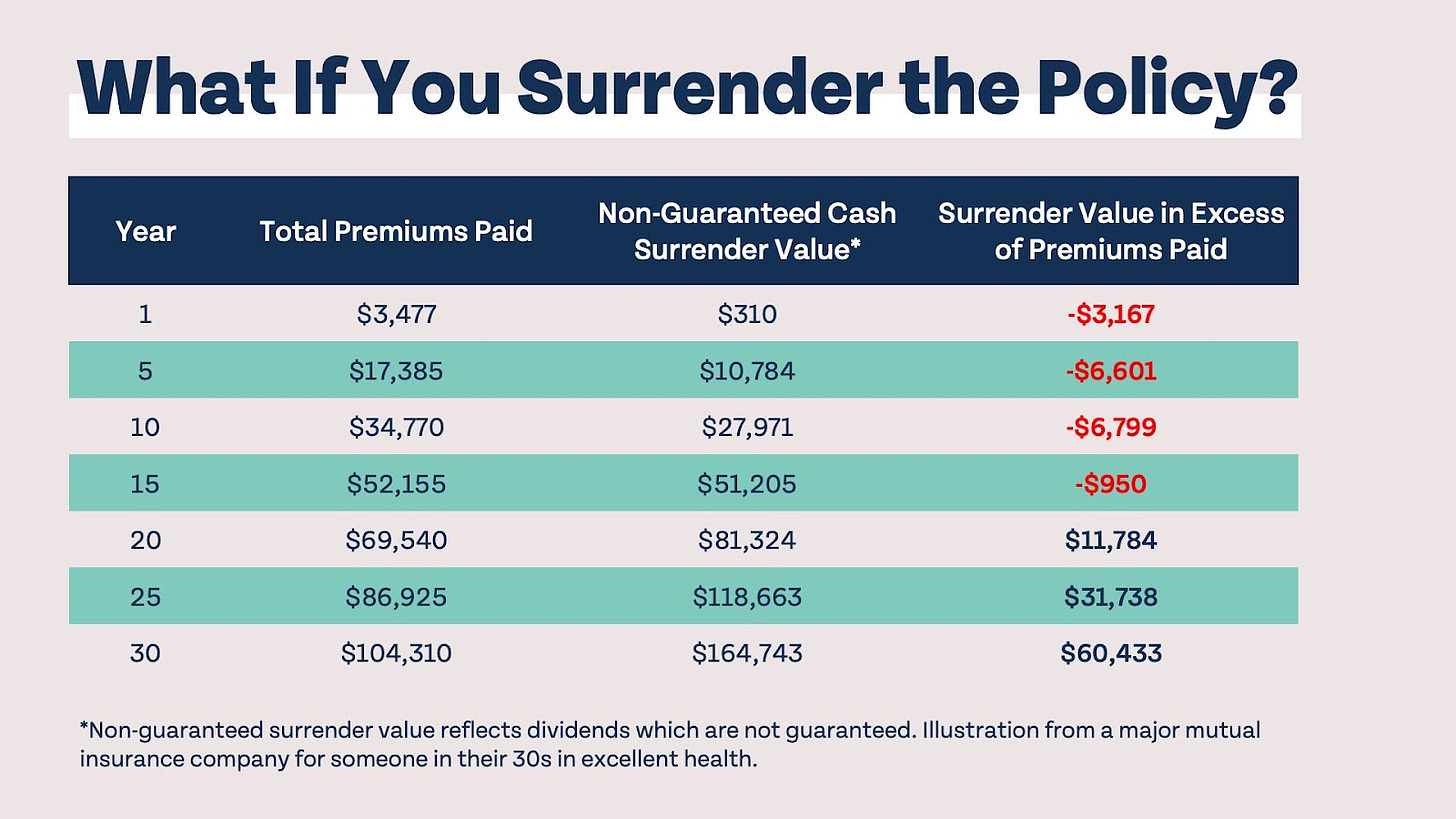

After one decade, the cash value has expanded to approximately $150,000. He secures a tax-free financing of $50,000 to begin a service with his brother. The plan lending interest rate is 6%. He pays back the car loan over the next 5 years. Going this path, the rate of interest he pays goes back into his policy's cash money value as opposed to an economic establishment.

Whole Life Concept Model

Nash was a money specialist and fan of the Austrian school of economics, which advocates that the value of items aren't clearly the result of traditional financial frameworks like supply and demand. Instead, people value cash and products in different ways based on their financial condition and demands.

One of the mistakes of traditional financial, according to Nash, was high-interest prices on loans. Long as banks established the passion rates and lending terms, people really did not have control over their very own wealth.

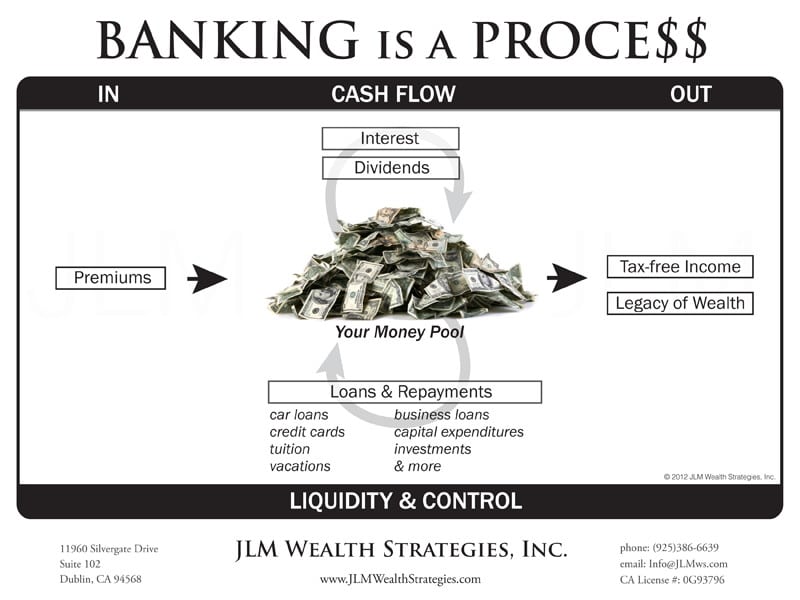

Infinite Banking requires you to possess your monetary future. For goal-oriented people, it can be the finest financial tool ever before. Below are the advantages of Infinite Banking: Arguably the solitary most helpful element of Infinite Financial is that it improves your cash flow.

Dividend-paying whole life insurance policy is extremely low risk and offers you, the insurance holder, a great bargain of control. The control that Infinite Banking uses can best be grouped into two categories: tax obligation advantages and possession securities.

Bank Infinity

When you use entire life insurance policy for Infinite Banking, you get in right into a private contract in between you and your insurance policy business. These securities may vary from state to state, they can include security from asset searches and seizures, security from judgements and security from financial institutions.

Whole life insurance coverage plans are non-correlated assets. This is why they work so well as the financial foundation of Infinite Financial. Regardless of what happens in the market (supply, real estate, or otherwise), your insurance coverage policy retains its worth.

Market-based financial investments expand wealth much quicker yet are subjected to market changes, making them naturally high-risk. What happens if there were a third container that used security but likewise moderate, surefire returns? Entire life insurance policy is that 3rd bucket. Not just is the price of return on your entire life insurance coverage policy ensured, your survivor benefit and costs are also guaranteed.

Here are its major advantages: Liquidity and ease of access: Plan financings offer prompt accessibility to funds without the constraints of standard bank finances. Tax obligation performance: The cash money value expands tax-deferred, and plan lendings are tax-free, making it a tax-efficient tool for developing wide range.

Infinite Banking Center

Asset security: In several states, the cash worth of life insurance coverage is secured from financial institutions, including an extra layer of monetary security. While Infinite Financial has its benefits, it isn't a one-size-fits-all remedy, and it comes with significant downsides. Right here's why it may not be the very best technique: Infinite Banking often calls for detailed policy structuring, which can perplex insurance policy holders.

Envision never having to fret concerning small business loan or high rate of interest rates once more. Suppose you could obtain money on your terms and construct wide range at the same time? That's the power of unlimited banking life insurance policy. By leveraging the money value of whole life insurance policy IUL policies, you can expand your riches and borrow money without depending on typical banks.

There's no set car loan term, and you have the liberty to choose the settlement timetable, which can be as leisurely as settling the lending at the time of fatality. This flexibility encompasses the maintenance of the finances, where you can select interest-only payments, keeping the financing equilibrium level and workable.

Holding cash in an IUL taken care of account being attributed rate of interest can often be better than holding the money on deposit at a bank.: You've constantly dreamed of opening your own bakery. You can obtain from your IUL plan to cover the preliminary expenses of renting a space, purchasing tools, and working with personnel.

Be My Own Banker

Individual financings can be acquired from conventional financial institutions and credit report unions. Borrowing cash on a debt card is normally really costly with yearly portion prices of interest (APR) frequently reaching 20% to 30% or even more a year.

The tax therapy of plan loans can vary significantly depending on your country of residence and the specific terms of your IUL policy. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy car loans are generally tax-free, offering a significant advantage. However, in other territories, there may be tax ramifications to take into consideration, such as possible taxes on the loan.

Term life insurance policy only gives a survivor benefit, with no money value accumulation. This suggests there's no cash money value to borrow versus. This post is authored by Carlton Crabbe, Principal Executive Policeman of Capital for Life, a specialist in offering indexed universal life insurance policy accounts. The info supplied in this post is for educational and informative purposes just and ought to not be taken as financial or investment guidance.

For funding police officers, the comprehensive policies imposed by the CFPB can be seen as cumbersome and restrictive. Initially, funding officers commonly argue that the CFPB's laws create unneeded red tape, resulting in even more documentation and slower loan processing. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) regulation and the Ability-to-Repay (ATR) needs, while focused on protecting customers, can result in delays in closing offers and raised functional costs.

{kind=link}

Latest Posts

Infinite Banking With Iul: A Step-by-step Guide ...

Be Your Own Bank: Cash Flow Banking Is Appealing, But ...

Becoming Your Own Banker And Farming Without The Bank