All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Overfunding your policy is merely another means of stating the goal should be to make the most of cash money and lessen costs. If you choose a common insurance coverage company, the cash will certainly have an ensured price of return, however the assured price will certainly not be adequate to both support the irreversible protection for life AND generate a consistent policy finance.

This does not suggest the technique can not work. It simply indicates it will certainly not be assured to work.

Any type of properly made policy will include making use of paid up additions and could additionally assimilate some non commissionable insurance policy to better decrease thew costs. We will certainly talk more about PUA riders later, yet recognize that an extensive conversation in this tool is impossible. To dive much deeper on PUA bikers and various other methods to lower fees will certainly require a thorough one on one discussion.

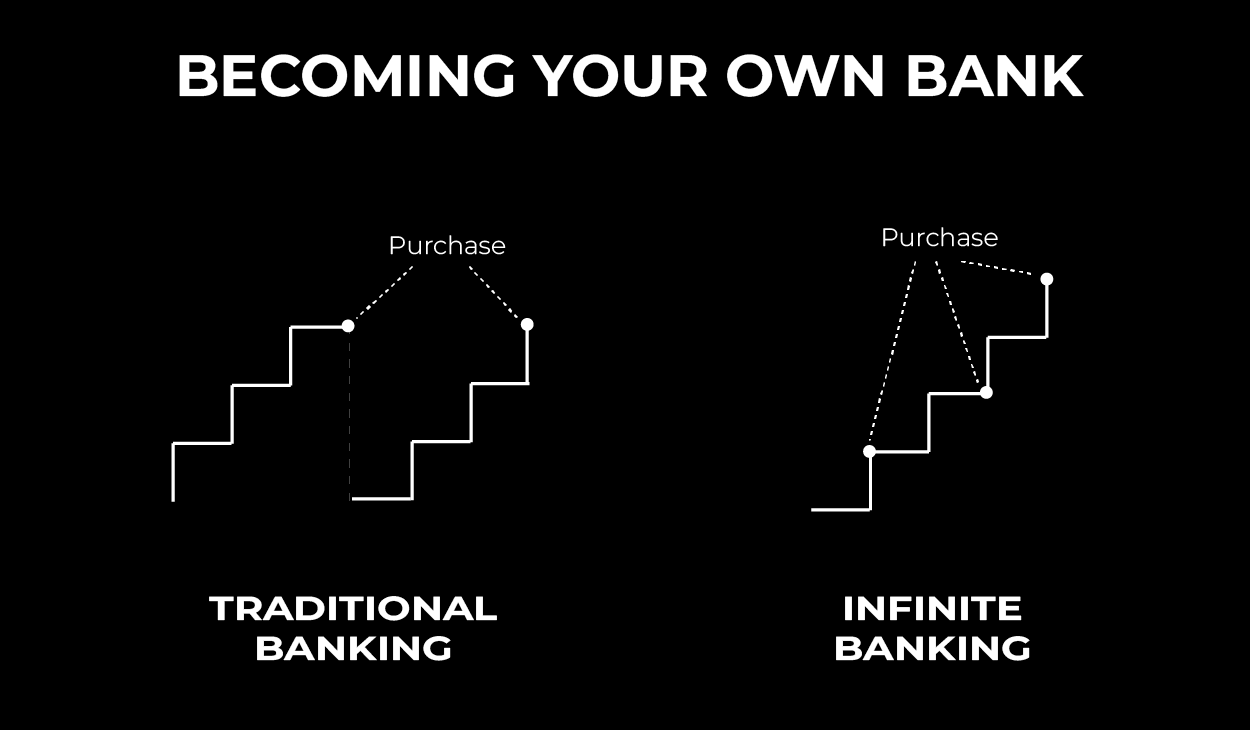

Currently what? You will unlock the power of leveraging equity from this individual bank. Your first step? Borrow versus your money abandonment worth. This is like using a cash cow that's been resting right under your nose. The appeal here depends on the flexibility it provides you can make major and rate of interest payments on any type of timetable wanted or pay nothing until able to make a balloon settlement.

Infinite Banking Concept Updated For 2025

Having the capability to regulate when and exactly how one pays back a loan is invaluable, enabling better flexibility than conventional loans use. Entire life insurance plans, unlike traditional loans, permit extremely flexible payment routines. The goal right here is not only to leverage however also handle this property properly while enjoying its advantages.

The biggest one? Tax-free growth within irreversible policies. Unlike term policies that give coverage just for set durations, cash-value policies are below to remain. One of the most substantial advantages of a cash-value policy is the tax-free growth within permanent policies. The taxman can not touch your money value development in a whole life plan.

That's not all. By leveraging PUA bikers efficiently, you can not just raise your plan's cash money value yet additionally its future returns potential. It's a win-win scenario. If you have an interest in adding PUAs to your plan, just get to out to us. We will certainly be able to provide support throughout the treatment.

The premiums aren't specifically pocket change, and there are prospective liquidity dangers included with this technique. I'll just go ahead and excuse half the room currently.

Whole Life Insurance Banking

This is regarding setting practical economic objectives and making informed choices based on those objectives. If done right, you could develop a different financial system using whole life insurance policy plans from mutual insurance companies providing long-lasting insurance coverage at low-interest rates contrasted to conventional lending institutions. Currently that's something worth thinking about. Overfund your Whole Life Insurance Policy policy to boost money worth and dividends, after that borrow versus the Cash money Give Up Worth.

Allows insurance holders to purchase sub-accounts, comparable to common funds. Traditional financial investments that supply prospective for growth and earnings. Can provide rental income and gratitude in worth. 401(k)s, IRAs, and various other pension offer tax obligation benefits and long-term growth possibility. High-income income earners can become their very own financial institution and generate substantial cash money circulation with long-term life insurance policy and the boundless financial technique.

For more details on the limitless financial method, start a discussion with us below:.

Be Your Own Banker Concept

If you do what everybody else is doing, you will probably wind up in the very same area as every person else. Dare to be various. Dare to come to be remarkable. Allow me reveal you just how. If you are battling financially, or are fretted concerning how you might retire someday, I believe you may locate some of my over 100 FREE helpful.

You an additionally get a fast overview of our approach by taking a look at our. If you require a that you can really sink your teeth right into and you are ready to stretch your convenience area, you have actually pertained to the right area. It's YOUR money. You remain in control.

Be My Own Bank - Your Journey To Financial Freedom Starts ...

Unfortunately, that funding against their life insurance policy at a greater rate of interest rate is mosting likely to cost even more cash than if they had not transferred the debt in any way. If you wish to make use of the strategy of becoming your very own lender to grow your wide range, it is necessary to recognize just how the approach actually works prior to obtaining from your life insurance coverage policy.

And incidentally, whenever you obtain cash always make certain that you can make more cash than what you need to spend for the car loan, and if you ca n'tdon't borrow the cash. Ensuring you can make more money than what you have borrowed is called creating free capital.

Totally free cash flow is much more essential to producing riches than purchasing all the life insurance policy worldwide. If you have inquiries concerning the credibility of that statement, research study Jeff Bezos, the creator of Amazon, and discover out why he believes so strongly in free cash money flow. That being stated, never ever ignore the power of owning and leveraging high cash value life insurance coverage to become your own lender.

Discover The Continuous Riches Code, a very easy system to maximize the control of your financial savings and reduce fines so you can maintain even more of the cash you make and build riches annually WITHOUT riding the marketplace roller-coaster. Download below > Example: "I believe it's the most intelligent way to collaborate with money.

Many people are losing money with regular monetary preparation. Even individuals that were "set for life" are running out of money in retirement.

Be Your Own Bank: 3 Secrets Every Saver Needs

Tom McFie is the creator of McFie Insurance coverage which assists people keep even more of the money they make, so they can have economic assurance. His most current book,, can be purchased here. .

They are paying you 0.5% interest per year which gains $50 per year. And is tired at 28%, leaving you with $36.00 You determine to take a lending for a new utilized vehicle, rather than paying money, you take a car loan from the financial institution: The lending is for $10,000 at 8% rate of interest paid back in one year.

at the end of the year the passion expense you $438.61 with a payment of 869.88 for 12 months. The Financial institution's Earnings: the difference between the 438.61 and the $36.00 they paid you is $402.61. In other words, they are making 11 times or 1100% from you all while never ever having any of their cash at the same time.

Like end up being the proprietor of the tool the bank. Let's keep in mind that they don't have any type of money invested in this formula. They just loaned your money back to you at a greater price.

Become Your Own Bank Whole Life Insurance

If you obtain you pay interest, if you pay money you are surrendering interest you might have made. In any case you are quiting passion or the prospective to obtain interestUnless you possess the financial feature in your life. After that you reach keep the automobile, and the concept and interest.

Visualize never ever having to fret about small business loan or high rate of interest once again. What happens if you could borrow cash on your terms and build wide range at the same time? That's the power of boundless financial life insurance policy. By leveraging the money worth of entire life insurance policy IUL plans, you can grow your riches and borrow money without relying upon traditional financial institutions.

{kind=link}

Latest Posts

Infinite Banking With Iul: A Step-by-step Guide ...

Be Your Own Bank: Cash Flow Banking Is Appealing, But ...

Becoming Your Own Banker And Farming Without The Bank